Open Banking represents a huge opportunity for building societies. From improving the effectiveness of lending through automation to providing the technical capability that underpins radically improved user experience, Open Banking can help building societies to maintain relevance in a fast-changing market.

For more information on how bud can help monetise open banking, get in touch with the team.

While banks have been the focal point for much of the open banking debate, I want to switch attention for a minute to building societies. Most don’t hold a day-to-day relationship with customers (unlike banks, where current accounts are a staple of their product suite). For building societies, business is built around deposit-taking and lending — something they have done extremely well for decades.

In the first quarter of 2019, building societies approved 120,626 mortgage loans, a 33% share of the 362,268 mortgage loans approved across the market in the period. Put into context, a one-third market share is hugely impressive. In a banking industry dominated by a handful of major players, the smaller operators are still comfortably punching above their weight.

The picture is almost identical when you look at savings. In the same 2019 period, deposits at building societies increased by £3.8 billion, a 35% share of the £10.9 billion across the market. Again, it highlights the success of these businesses within a crowded market. So why should they bother looking at something like open banking?

In short, the potential for these businesses to improve their position, growing their customer base and revenue is huge — built around new regulation and, crucially, changing customer demands.

First, a quick background on open banking. Customers can now request that their banking data be sent to companies that will put it to good use (in this case, banking data means transactional data). It doesn’t take long to think of a few use cases for consumers, like the ability to check whether they are overpaying their bills, or to pull all their pension plans together if they change jobs.

Effective lending (fewer maybes, more decisions)

Automation is partly the key to creating better margins: reduce costs and maintain competitive pricing and the business will see positives change in profit. In order to maximise the benefit of automation, organisations should look at the most costly processes and see how they can introduce technology to help free up resources.

In lending, more often than not, ‘maybes’ are costly. The level of risk a lender is willing to take changes institution by institution. If you could increase knowledge about a user — or gain access to new data points that will allow you to make a more informed ‘yes’ or ‘no’ — you can start to limit the ‘maybe’ assessments.

One open banking use case in this context is the ability to unlock transactional data. This transactional data is up to date and contains information pertinent to responsible lending decisions. With the right enrichment, from Bud’s enrichment services, lenders can speed up decision making and in certain cases make more informed decisions and reduce the cases needed for manual underwriting.

Maintaining relevance in a changing market

It’s no secret that customer expectations around financial services are changing and, like everyone else, building societies aren’t immune from this. End-to-end journeys, from origination to fulfilment, are now expected by consumers in the digital space; it’s simply no longer sufficient to survive on a great product without the desired user experience to accompany it.

These changes are particularly prominent within young people (a demographic Bud studied closely in its first Futureproof series). As well as being less inclined to carry out their financial interactions in-branch, they are also evolving into major players in the spending and saving worlds. While wages continue to stagnate, millennials are looking to diversify their revenue streams — and almost 1 in 2 are considering starting their own business, or have done already.

Bud has focused on building easy-to-implement technology that resonates with this customer base, providing them with seamless user journeys as they look to improve their sense of financial confidence. From budgeting services to credit score optimisation, we’ve built our platform to solve end-customer needs.

Going beyond lending and deposit-taking

We know that the building society business model is built around lending and deposits but, as these changes in consumer attitudes and technological capabilities emerge, they will need to adapt to survive. This doesn’t mean a change in strategy — almost all building society CEOs agree they need to focus on what they are good at to fend off new challengers — but there is an easy way to add to your product line without distracting from the core.

This is where open banking culture goes beyond the mandated compliance requirements and opens up something new entirely. Using APIs, the marketplace banking model has allowed financial service providers to distribute the products of third parties via their platforms — meaning customers can be served in more complete ways, and revenue streams can be diversified.

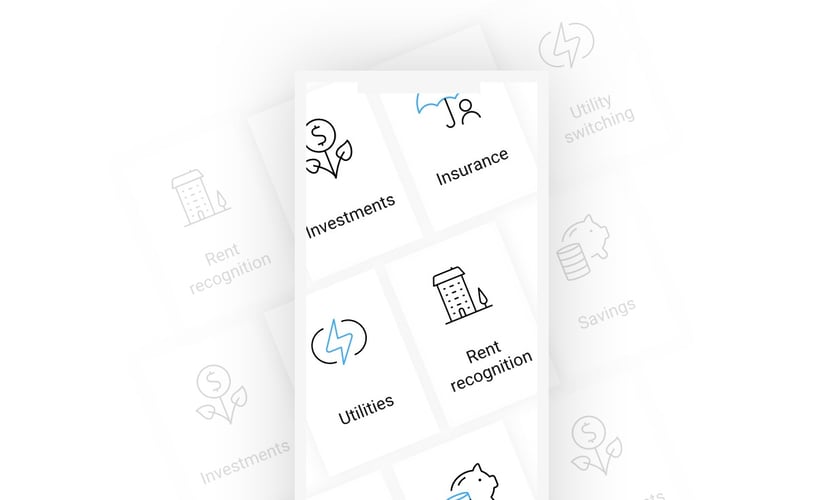

For building societies, this could mean offering household insurance after a mortgage product, including an investment service for customers willing to take on risk as part of their long-term planning or providing an integrated currency exchange partner for customers with a mortgage or school payments overseas. With Bud’s marketplace, one simple integration can open up these new frontiers.

Unlocking the potential of open banking

For more use cases or for more information on how to commercialise open banking, get in touch with the team.